A Smoother Ride

A Smoother Ride

- May 3, 2023

Well I’m accustomed to a smooth ride

Or maybe I’m a dog who’s lost it’sbite

I don’t expect to be treated like a fool no more

I don’t expect to sleep through the night

Some people say a lie’s a lie’s a lie

But I say why

Why deny the obvious child?

-Paul Simon, “Obvious Child”

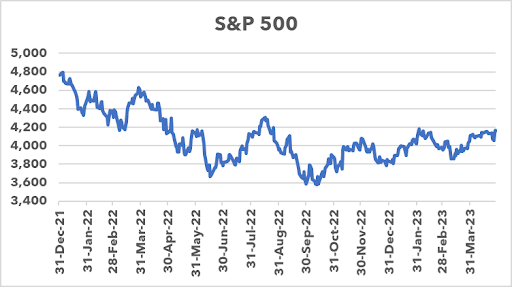

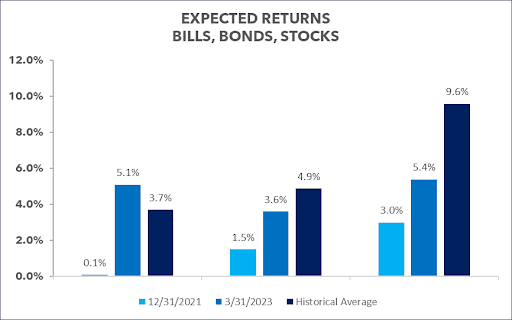

Similarly, expected returns in the stock market have improved markedly, but remain well below historical averages. After generating returns above historical averages for the past 7-to-10 years, the market stands poised to generate below average returns over the next decade.

There are two ways that 5.4% can get back to the historically observed 10% return. Firstly, earnings growth can simply outpace S&P 500 price appreciation to the point that the price on the market is eventually justified by the fundamentals. Or, the market can take a significant downturn to get much cheaper quickly. For example, if the S&P 500 fell by approximately -30% before the end of the year, the expected return would rise to the historical average. How likely is it that the market would fall by 30% versus slowly growing into its current, inflated price? The stock market fell by that much or more in the DotCom Crash of 2001; the Great Financial Crisis of 2008; and the Covid crash of 2020. The ending of 13 years of ZIRP seems equally momentous.

We don’t know for certain which path the market will take to start to offer higher returns. Or, even if it ever will. Butwe do know that the risk that it will fall by an unacceptable amount for our investors remains above average.

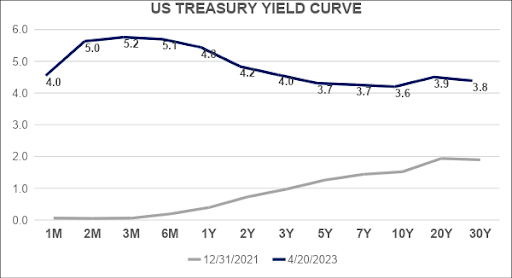

Investors maintaining half of their normal stock market exposure makes sense to us. Being able to generate 5% in US Treasuries with virtually no risk and almost no volatility is superior to us than attempting to earn the same in the stock market with much higher volatility.The stock market’s optimism disagrees with the pessimism of the bond market. We are inclined to believe the bond market. But we are not doctrinaires. We are open to the idea that the stock market is correct. Consequently, it makes sense to maintain some exposure to the stock market, especially when that exposure is governed by trend. Historically, trend following has done a good job of getting out of the market early during pronounced corrections.

It is historically unusual that you can receive the same expected returns in 3-month US Treasury Bills as you can in the S&P 500. We do not expect this situation to last for very long. Until then, it’s wise for investors to tread carefully. And demand greater returns for taking more risk.